The book in three sentences

Doing well with money has little to do with how smart you are and a lot to do with how you behave. That’s the whole book for me.

Wealth is what you don’t see, and your savings rate matters far more than your income or your returns.

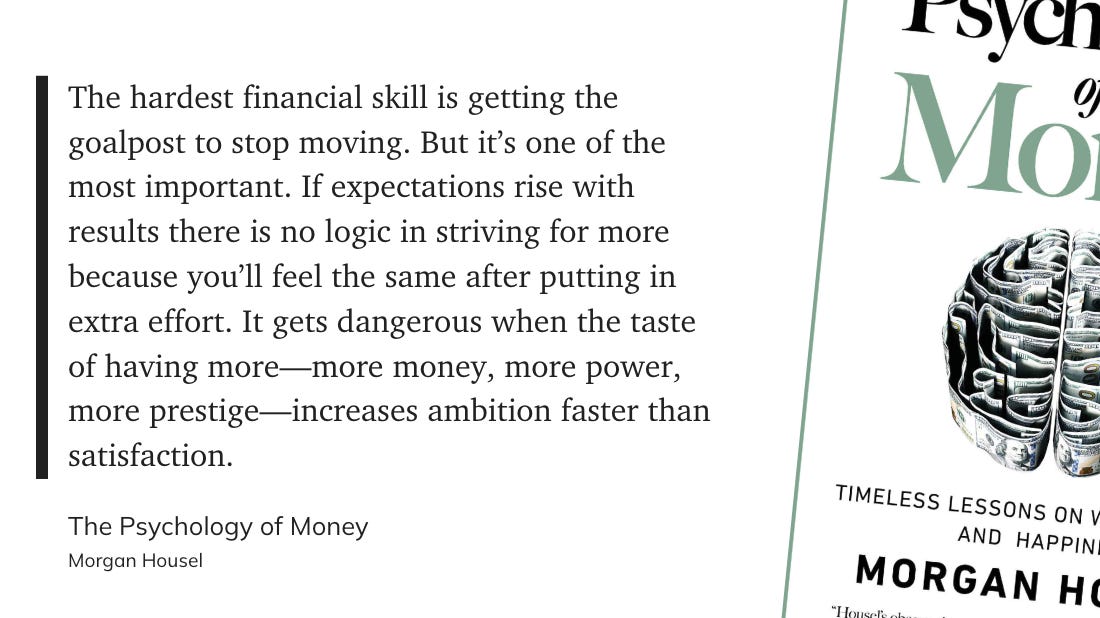

The edge isn’t picking winners, it’s endurance. Staying reasonable, leaving room for error, and never interrupting compounding.

Why I Picked It Up

I came back to this book right after the editorial team at Moneywise announced they would be interviewing Morgan Housel, during the same weekend, I finally had a chance to visit Monet at the Musée d’Orsay.

It’s the one I recommend to anyone walking into personal finance for the first time, and the one I’d put in every college curriculum. The kind of read where you keep nodding because he keeps naming things you already half-knew. Most finance books teach you the math, yet Housel reminds us of the human side in an easygoing style, making it one of my favorites in the category.

Wealth is what you don’t see

Ronald Read swept floors and pumped gas in rural Vermont, never earned more than minimum wage, wore very simple clothes, and drove a beat-up car. When he died at 92, his estate was worth $8 million, most of it left to the local hospital and library. No lottery, no inheritance. He just saved what little he could, bought blue-chip stocks, and waited for decades.

A few months earlier, another man named Richard had been in the news. Richard Fuscone was everything Read was not — Harvard MBA, Merrill Lynch executive, retired in his 40s, an 18,000-square-foot home in Greenwich with eleven bathrooms and a see-through cover over the indoor pool. Then 2008 hit. High debt, illiquid assets, and the mansion was sold at foreclosure. “I currently have no income,” he told a bankruptcy judge.

The janitor beat the banker, not on intelligence, education, or income, but on basic personal finance habits and common-sense behavior. That’s the whole book in two lives. The win condition has nothing to do with being a genius but being consistent long enough that compounding can do the work.

Wealth is what you don't see, the Porshe not bought, the first-class upgrade declined, the Channel bag left in the store, the appartment in Costa del Sol that didn’t close. Wealth, by definition is hidden, it’s capital that hasn’t been converted into stuff.

When most people say they want to be a millionaire, what they often mean is “I’d like to spend a million dollars,” which is literally the opposite of being a millionaire. Most of what looks like wealth is just spending. The genuinely wealthy people are the ones you can’t pick out of a crowd.

Savings rate is king

The oldest name for the discipline is “pay yourself first”, which will always remind me of The Richest Man in Babylon’s parable “a part of what you earn is yours to keep.”

This is the one I live by for as long as I can remember and attribute much of my investing success to. For every invoice, investments and savings come off the top, before the lifestyle catches up to the income, then the rest is what’s free to spend, guilt-free.

Growing up in Brazil after the 1994 first impeachement and economic crisis conditioned me to the reality of “living according to our means” and Morgan's experience forces you to reflect how building wealth has surprisingly little to do with my income or investment returns, but the gap between what I earn and what I spend, which is comforting to think that is far more under my control than the next great stock pick.

Expanding that gap is two-fold: taming a wild lifestyle creep is key because you spend less by wanting less, and you want less by caring less about what others think, that's optimizing the bottom line.

Optimizing the top line is the healthy ambition to make more. I empathize people's journeys are different, but for me, negotiating better contracts over the years became the bedrock to my financial independence.

Time is the multiplier

The first rule of compounding is to never interrupt it unnecessarily.

Most of Buffett’s net worth was accumulated after his 60s. He’s a great investor, but his real superpower is that he’s been one for three-quarters of a century. If he’d retired at 60, almost no one would know his name, and that’s the lesson, especially for the retail investor, our performance doesn't come from what we buy or sell, it comes from what we hold. The main activity is holding.

This is also why endurance matters more than peak returns. Housel, talking with Howard Marks, calls it strategic mediocrity, being willing to operate below your potential year over year so you can still be in the game in year thirty.

The mathematically optimal portfolio is worthless if you can’t stomach steep drawdown. A “sleep well at night” portfolio is, in the long run, the highest-returning portfolio, because it’s the one you don’t act emotionally and abandon at the worst moment.

Things I keep doing because of this book

Pay myself first. Savings come off the top, before the lifestyle catches up to the income.

Keep a healthy margin of safety. Cash reserves that cover five months of living expenses, allowing me to stay invested when markets get loud.

Refuse leverage. I chose to live this life debt-free with no hard assets, and I sleep better every night because of it.

Hold for decades. The compounding clock starts the moment I stop interrupting it.

A Note from me

Morgan Housel became my favorite personal finance writer. I have read all his books to date, and every single Collab Fund thought leadership piece. Probably my most recommended book to people asking “where to start?” when I start obsessing about the world of finance.

What to Read Next

Investing has been solved, but it's not easy because our human emotions get in the way of our success. I attribute a lot of my success with money to the fact that I started the compounding process early in life, never chased get-rich-quick schemes, kept it simple, boring, and diversified. If that sparks your curiosity, consider reading my piece on winning with investing.

Set aside a part of all you earn before a single coin goes anywhere else, and let it compound while you sleep. A hundred years later, the phrase is everywhere, which is the surest sign it works.